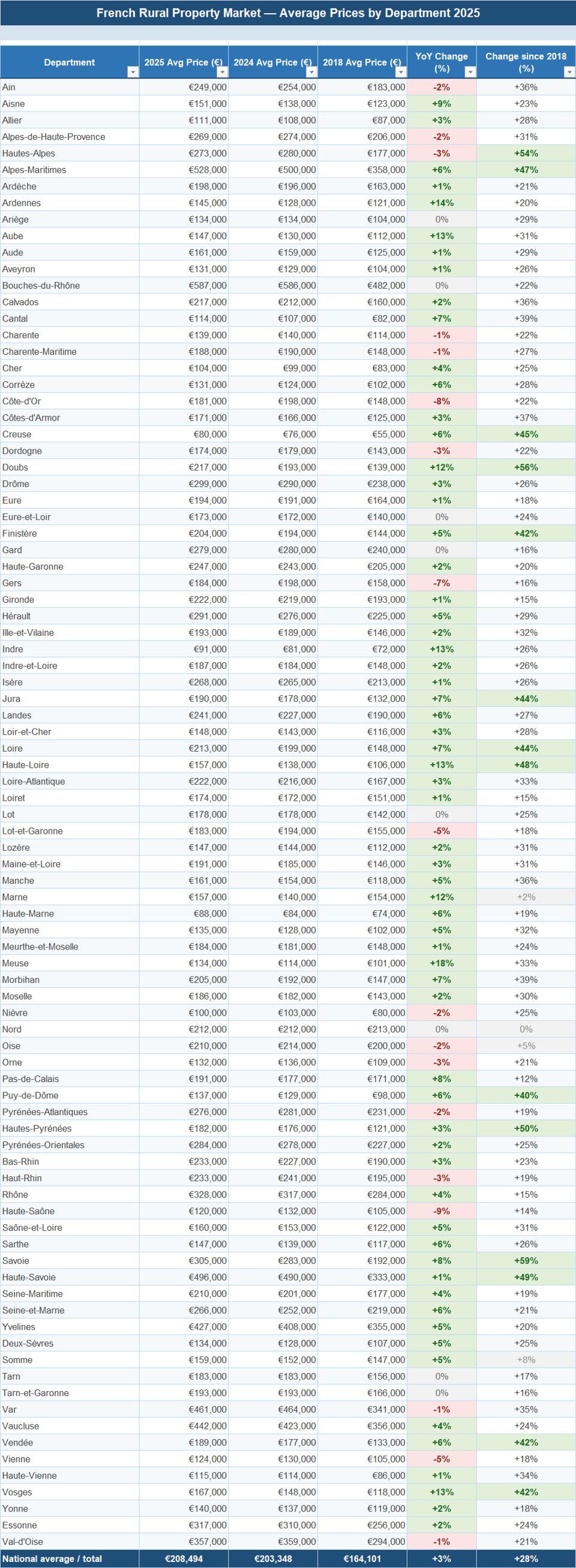

The French rural land agency SAFER has published its annual review of the market for rural property for 2025.

France's rural residential property market ended 2025 in a state of cautious recovery, with the national average price for existing houses standing at approximately €202,000 — a net increase of around 2–3% on the year.

As is often the case, however, the headline figure masks a mixed picture, with rapid price growth in some of the country’s more affordable departments contrasting with a softer market in traditionally expensive areas.

In addition to an analysis of the market for the year, SAFER published figures tracking the movement in prices since 2018.

They show that most departments have appreciated by 20–50% over seven years, with a cluster of high-demand coastal and Alpine markets delivering gains well in excess of 50%. Only a handful of markets in areas of structural population decline or economic weakness have failed to keep pace.

Of the 86 departments for which data is available, 57 recorded price increases in 2025, 20 recorded falls, and 9 were unchanged. This marks a clear improvement on 2024, when falling or stagnating markets were more widespread.

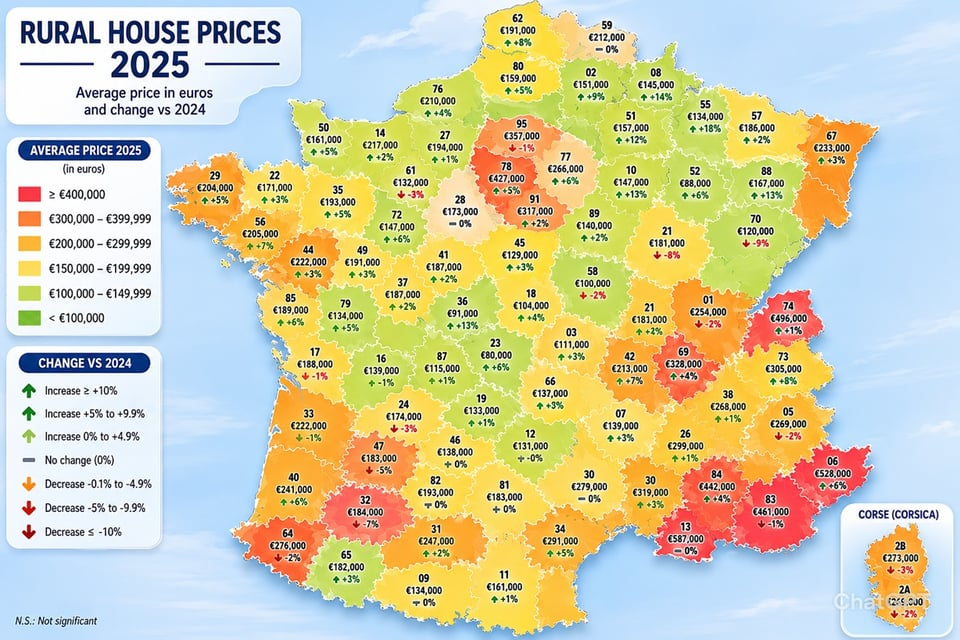

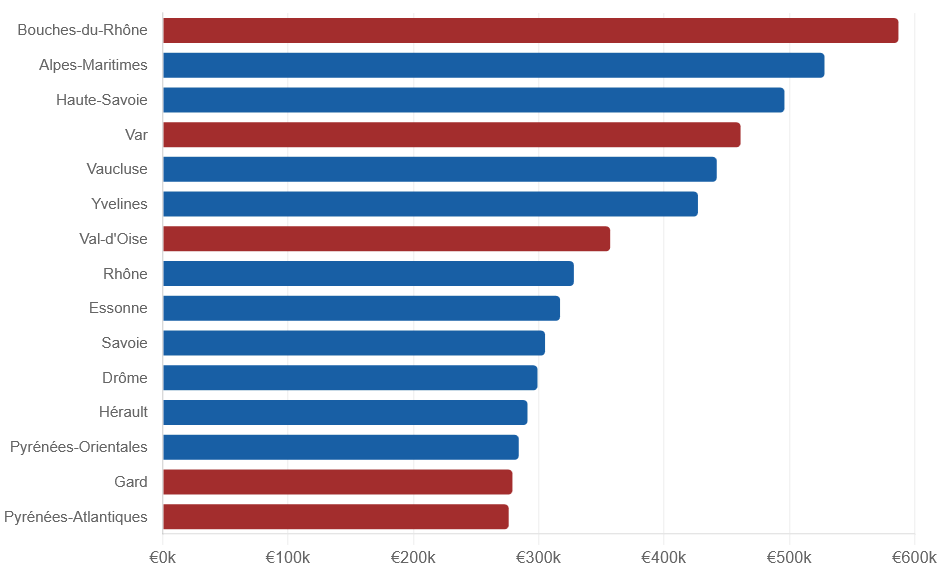

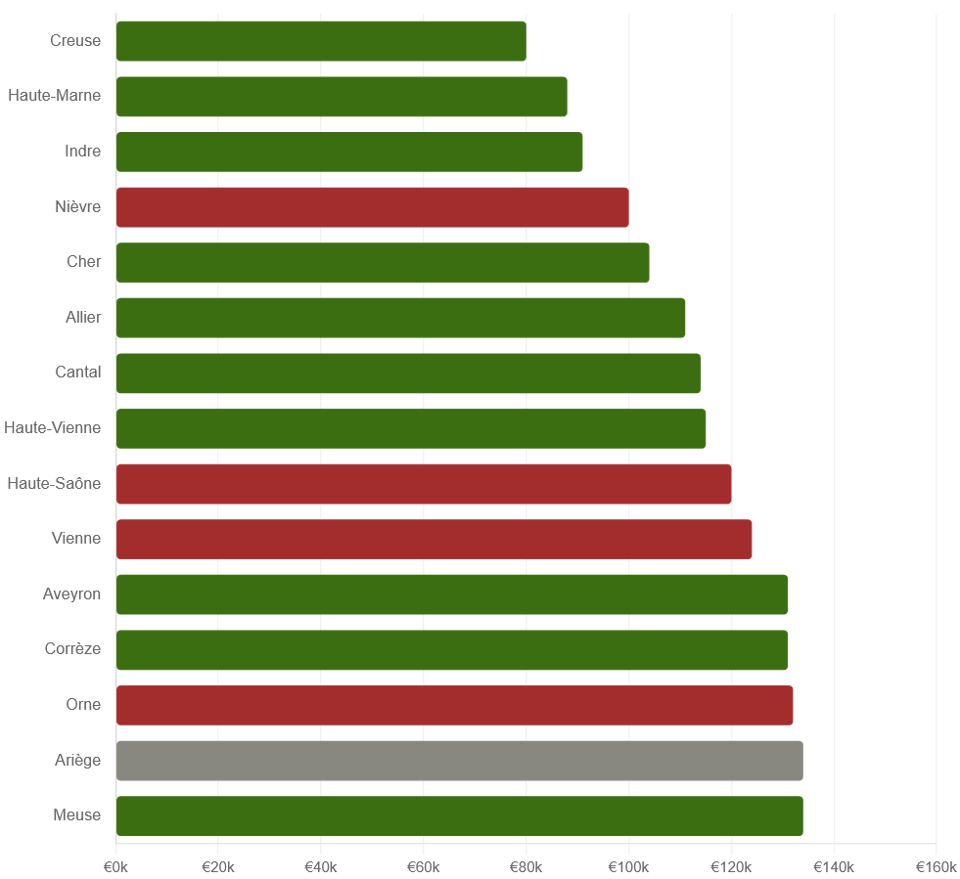

A cartographic representation of the 2025 figures is shown below, followed by charts showing the 15 most and least expensive departments.

The 15 most expensive departments:

The 15 least expensive departments.

Regional Analysis

Grand Est

Grand Est was the stand-out region of 2025, posting growth across almost all its departments. Meuse (+18%), Ardennes (+14%), Aube (+13%), Vosges (+13%), Marne (+12%) and Doubs (+12%) all feature in the national top performers.

The common thread is that these markets were historically inexpensive, had seen limited price growth in the period 2018–2023, and are now attracting buyers from Paris and the Île-de-France who find the combination of value, quality of life and improving rail connections increasingly compelling.

Alsace is a partial exception (Bas-Rhin +3% and Haut-Rhin −3%) reflecting its existing status as a premium regional market and cross- border dynamics with Switzerland and Germany.

Auvergne-Rhône-Alpes

The Auvergne-Rhône-Alpes is a region with marked contrasts in the market. At the top end, Haute-Savoie (€496,000) and Savoie (€305,000) only appreciated marginally, but continue to attract domestic and international buyers seeking mountain property, underpinned by structural scarcity and sustained demand from wealthy urban buyers.

At the interior, the Massif Central departments Loire (+7%), Rhône (+4%), Haute-Loire (+13%) and Allier (+3%) all recorded solid growth in 2025, driven by urban overspill from Lyon and Clermont-Ferrand. By contrast, Ain (−2%) and Haute-Saône (−9%) reflect cooling demand in departments that benefited heavily from the pandemic surge but now face normalisation.

Provence-Alpes-Côte d'Azur

PACA remains the most expensive region for rural property in metropolitan France. Bouches-du-Rhône (€587,000) and Alpes-Maritimes (€528,000) stand at the top of the national table, reflecting the enduring premium attached to Mediterranean coastal and hinterland locations.

At those price levels, it is perhaps unsurprising that momentum has softened, with Bouches-du-Rhône unchanged in the year, Var fell −1%, and Hautes-Alpes fell −3%. Vaucluse (+4%) and Alpes-Maritimes (+6%) performed more strongly.

Nouvelle-Aquitaine

Nouvelle-Aquitaine is the region where the 2025 data paints the most cautious picture.

Several departments that were star performers during the 2020–2022 period are now recording falls or stagnation. Dordogne (−3%), Lot-et-Garonne (−5%), Gers (−7%), Charente (−1%) and Charente-Maritime (−1%) all declined.

Part of the explanation lies in reduced demand from international buyers (especially British purchasers), but also to the end of the post-Covid remote-working surge that drove urban buyers southward. Gironde (+1%) and Landes (+6%), which benefit from Bordeaux spillover and Atlantic beach proximity respectively, were more resilient.

Bretagne and Pays de la Loire

Brittany and the Loire region continue to perform steadily, driven by consistent domestic demand, a large and active retirement buyer market, and growing interest from international purchasers (particularly British and American) attracted by price-value ratios unavailable further south. Morbihan (+7%), Loire (+7%), Loire-Atlantique (+3%), Finistère (+5%) and Côtes-d'Armor (+3%) all posted positive returns.

Loire-Atlantique and Morbihan were both very active markets, each recording 2,400 transactions in the year. Prices here typically range from €160,000 to €225,000, sitting in a tier that remains accessible to a wide buyer pool.

Normandy

Normandy does not generate dramatic headlines in the review. It neither surged wildly during the pandemic boom nor corrected sharply afterwards — but it has delivered consistent and genuine growth since 2018, with Calvados and Manche both up over a third in seven years.

In the year, Seine-Maritime (+4%), Manche (+5%) and Calvados (+2%) were all positive, driven by proximity to Rouen and Caen, active demand from Parisian second-home buyers, and — in the case of the Manche coast — continuing interest from British buyers for whom the Channel crossing remains the most direct route into France. Eure (+1%) was essentially flat. Orne (−3%), landlocked and with a smaller buyer pool, gave back some of its pandemic-era gains.

Long-Term: 2018 to 2025

Taking the national sample as a whole, the report shows that the average rural house price has risen from approximately €166,000 in 2018 to €202,000 in 2025 — an increase of around +22% in nominal terms.

This average, however, conceals a range of outcomes spanning from essentially zero growth (Nord: 0%) to extraordinary appreciation (Savoie: +59%, Hautes-Alpes: +54%, Creuse: +45%).

Savoie's +59% over seven years reflects not just the Alpine tourism premium but the increasing demand for year-round mountain living among wealthy urban buyers from Lyon, Geneva and Paris.

Creuse (+45%) has historically been a distressed rural market, but has experienced a genuine recovery in demand as the pandemic accelerated what had previously been only a trickle of buyers drawn by exceptional value. With average prices around €80,000, it remains one of the cheapest rural property markets in Western Europe.

A small number of departments have recorded limited gains since 2018, reflecting structural rather than cyclical challenges. Nord (0%) is the most striking, pointing to persistent demographic and economic pressures in a market dominated by industrial towns rather than rural countryside.

Cumulative consumer price inflation in France for 2018-2025 was nearly 20%, so most departments have shown a positive return over this period, albeit in most cases not a substantial one.

Related Reading: