Two new reports from housing market commentators suggest that the rebound which began in 2025 is losing momentum, with both organisations warning that the market is entering a more challenging phase after a brief period of stabilisation.

The reports are from the Fédération Nationale de l'Immobilier (FNAIM), the national association of estate agents, and BPCE L'Observatoire, the research arm of one of France's largest banking groups.

FNAIM's latest assessment describes the market as a "convalescent patient on the verge of relapse." The federation argues that while falling mortgage rates helped revive activity last year, a combination of economic uncertainty, supply shortages and international tensions has interrupted the recovery.

"The market had regained some colour thanks to lower borrowing costs and the gradual return of buyers," said FNAIM president Loïc Cantin. "But economic, international and political uncertainties have interrupted that dynamic."

The French housing market suffered one of the sharpest contractions in its modern history between 2021 and 2024. Rapid increases in borrowing costs, tighter lending criteria and declining affordability caused sales to collapse by roughly one-third.

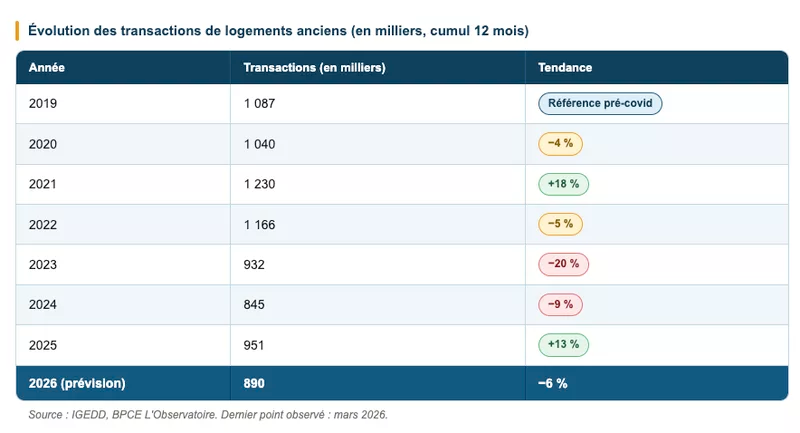

The graphic below shows the sales figures for the years 2019 and forecast for 2026.

By the end of 2024, annual existing-home sales had fallen to around 845,000 transactions, compared with more than 1.2 million at the market peak in 2021.

The recovery began in earnest during 2025, supported by falling interest rates, and by a gradual return of buyer confidence.

Then came a sudden reversal, which coincided with the conflict in the Middle East.

Figures from the government show that housing transactions in March fell by 8% compared with March 2025. Over the twelve months to the end of March, total sales stood at approximately 951,000, well below the levels recorded during the post-pandemic boom. The forecast for 2026 is sales of 890,000.

"This slowdown did not begin with the geopolitical crisis," BPCE notes. Because there is typically a three-month gap between signing a preliminary sales agreement (compromis de vente) and completion, the decline in March transactions reflected a deterioration in buyer sentiment that had already begun during late 2025. In short, the geopolitical backdrop has compounded an existing fragility rather than created it.

The recovery of 2025 was built largely on cheaper borrowing, and that support is now fading.

BPCE forecasts that mortgage rates will edge higher through the remainder of 2026, reaching approximately 3.43% by the final quarter of the year. French buyers remain highly dependent on mortgage finance — far more so than their British or American counterparts, making the housing market unusually sensitive to the cost of credit.

BCPE state that the composition of borrowing is also shifting in ways that reveal deeper structural stress. “While first-time buyers remain active and now account for 47% of all new mortgage lending, second-time buyers and investors are retreating in significant numbers.” Investor borrowing has fallen sharply compared with pre-rate-hike levels, and wealthier owner-occupiers who are less dependent on leverage are increasingly dominating activity.

FNAIM describes the consequence bluntly: "The residential ladder is broken."

Beyond the national trends, the analysts point to a growing divergence between regional markets that makes aggregate figures increasingly misleading. Local economic conditions, employment growth, demographic dynamics and housing supply are exerting a greater influence on prices and volumes than broad national cycles.

In Paris and the wider Île-de-France region, affordability constraints remain acute despite a modest improvement in sales activity. Average prices in the capital have fallen from their 2020 peak but remain among the highest in Europe relative to local incomes, limiting the pool of potential buyers even in a lower-rate environment. By contrast, parts of western and southern France — notably the Atlantic coast, the Occitanie region and parts of Auvergne-Rhône-Alpes — continue to benefit from sustained demographic growth, internal migration flows, and demand for lifestyle-oriented housing.

As a result, analysts increasingly speak of "French housing markets" in the plural rather than a single national market

Related Reading: