The national association of estate agent (FNAIM) paints a mixed picture of a genuine revival in sales, but persistent obstacles that threaten to weaken this momentum.

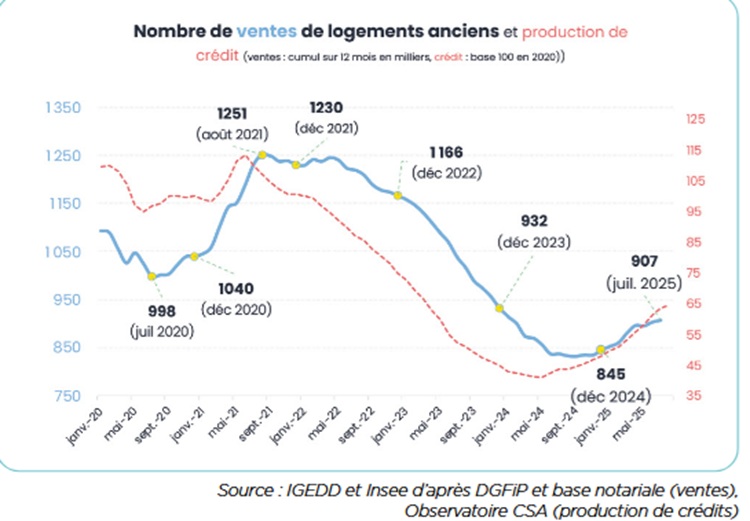

According to the report, the volume of transactions in the existing homes segment has picked up, with 910,000 sales recorded by the end of July, an +8.7% increase year-on-year. FNAIM anticipates that this trend will continue: sales could reach between 925,000 and 930,000 units by the end of the year.

This rebound comes after a significant decline in sales in recent years and reflects renewed dynamism in the market. However, the report stresses that the recovery is not accelerating rapidly. Since spring, the rebound has been moderate, held back by several structural factors.

One of the main sources of fragility in the market remains economic and political uncertainty. The report highlights the climate of distrust weighing on buyers: purchasing decisions are being delayed, or even postponed, due to the lack of visibility on fiscal and regulatory policies.

The increase in transfer/stamp duty, which rose in most departments in 2025, raised the entry cost for many buyers.

At the same time, the stabilisation of mortgage interest rates limits room for improvement. After a sharp decline, rates have stabilised around 3% according to the Observatoire CSA/Crédit Logement, a level that no longer supports an increase in real estate purchasing power.

Prices

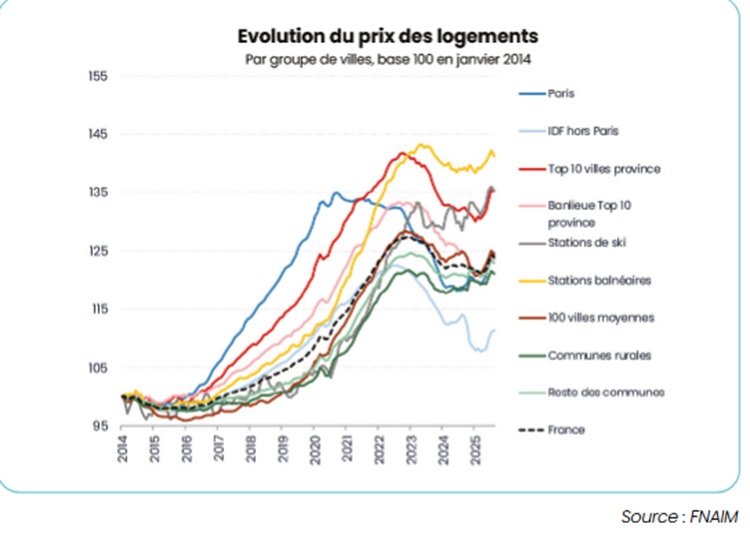

On prices, the rebound is present but timid. After an average drop of -5% nationwide, prices have begun to edge upward, by around +1% to the year to September 2025.

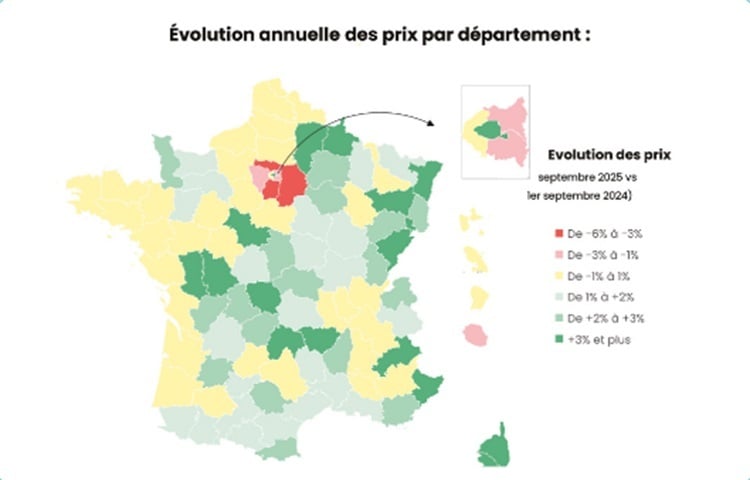

This upturn remains uneven across regions. In some major-city suburbs, prices are still falling (for example −2.3% in the Paris suburbs). Conversely, rural areas are seeing a notable rise (+1.9% year-on-year), indicating renewed interest in these territories.

The following graphic shows the movement in prices in different geographic sectors since 2014.

The following graphic shows the average movement in prices by department in the year to September 2025.

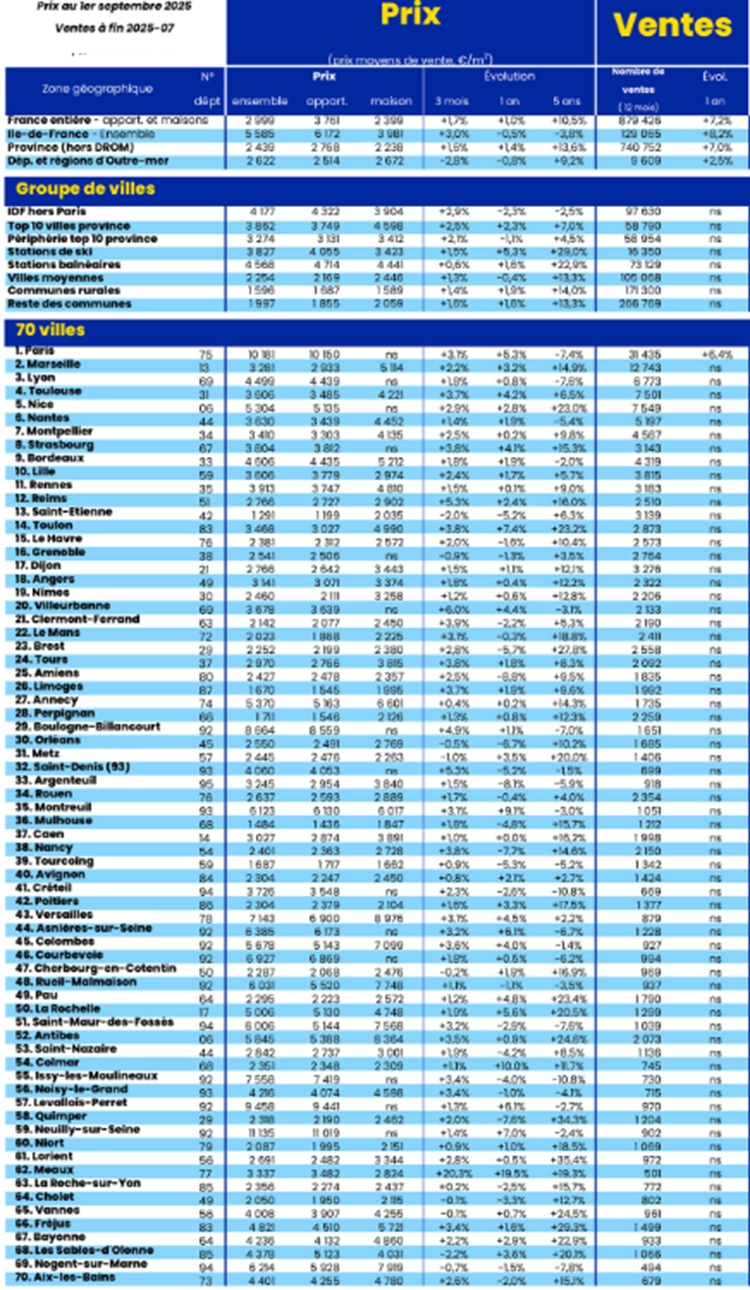

The following graphic shows the prices in the top 70 towns, as well as the average movement in prices, for the year to September 2025. Our apologies for the quality of the graphic.

And as we have stated previously on these pages, there are many different housing markets in France, so as Dan Newton of estate agents Agence Newton states: “While the national figures are certainly useful, particularly if you’re looking in a rural area it’s best to treat them as a guide only.”

A key point highlighted in the report is that inflation is now under control, having been up to 7% in 2022/3. It now stands at around 1%, well below the eurozone average (around 2.1%).

Although low inflation will support purchasing power and macroeconomic stability, the report also points out that growth is low. According to the Banque de France there will be GDP growth of 0.7% in 2025, 0.9% in 2026, and 1.1% in 2027.

In this context, the real estate market’s recovery could stall if household and investor confidence is not strengthened.

For FNAIM, the real question is now political: without a clear and stable framework, the positive signals may not be enough to transform the rebound into a lasting trend. Loïc Cantin, president of FNAIM, calls for a “true confidence shock.” The main components of this shock are fiscal stability, more support for renovation of the older homes, making the rental market more attractive and offering more assistance to fist-time buyers.

Without these measures, FNAIM warns, the current recovery risks remaining superficial, hindered by mistrust and a lack of visibility.

Related Reading: