Earlier this week the notaires published their annual review of the housing market.

In their eagerness to be first out of the blocks, the figures are only to Sept 2024, although with extrapolations to the year end based on contracts signed in the final quarter.

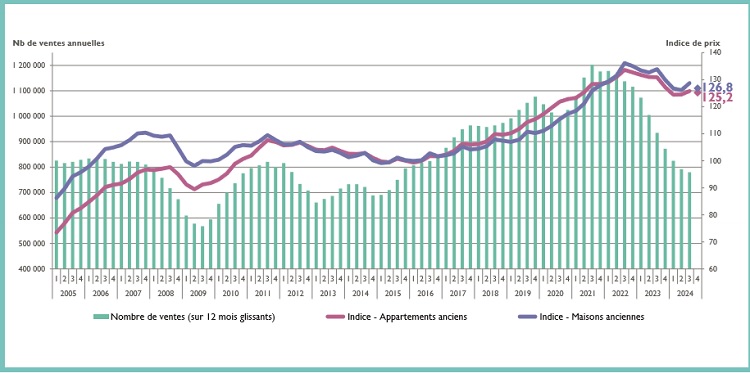

The notaires report that to the end of Q3 there were 780,000 sales on an annualised basis, a fall of 17% over 2023 (935,000). The volume of transactions over the 12-month period is similar to that observed in 2015 (790,000).

Departments with a notable fall in sales were Charente Maritime (-22%), Gironde (-23%) and Pyrénées-Orientales (-23%).

The graphic below shows the trend in sales since 2005. As can be seen, sales this year have been in line with the historic average, with the post-Covid period an exception.

The graphic also shows the movement in the price index over the same period. In Q3 the index corresponds to that observed in Q1/22 for properties outside of the Ile-de-France, and to Q4/20 for properties in the Ile-de-France.

Prices in Q3 remained stable compared to Q2, but over a year prices have fallen by a national average of -3.9%. In the Ile-de-France prices fell by -5.4%, whilst in the regions by an average of -3.6%.

The notaires forecast that to the end of the year there will be some improvement in the market, with prices falling only marginally in the regions and by around -3% in the Ile-de-France.

Inevitably there are variations around the country, although the notaires provide no detailed figures on the performance of the market in rural areas. Those figures will be available next year.

In metropolitan areas, there have been significant price falls over the year in Reims (-8%), Saint-Etienne (-8%), Bordeaux (-9%), and Nantes (-10%). More moderate falls of around -4% occured in Nice, Toulon and Montpellier.

Longer Term Trends

Over the past 5 years the trend has been upwards. Price rises up to +10% have occurred in Paris (+3%), Bordeaux (+5%), Reims (+5%), Toulouse (+7%), Nantes (+8%), Grenoble (+10%) and Saint-Étienne (+10%).

Price rises between +10% and +20% have occurred in Orléans (+12%), Strasbourg (+12%), Lille (+16%),

Dijon (+16%), Marseille-Aix-en-Provence (+17%), Rennes (+17%) and Lyon (+19%).

Rises above +20% have occurred in Le Havre (+21%), Toulon (+22%), Nice (+22%) and Montpellier (+24%) and Marseille (+31%).

Over a 10-year period rises of over 20% have occurred in several agglomerations - Dijon (+23%), Lille (+25%), Le Havre (+27%), Strasbourg (+28%), Marseille-Aix-en-Provence (+29%), Nantes (+30%), Montpellier (+32%), Toulon (+32%), Rennes

(+34%), Lyon (+34%) and Bordeaux (+37%).

International Buyers

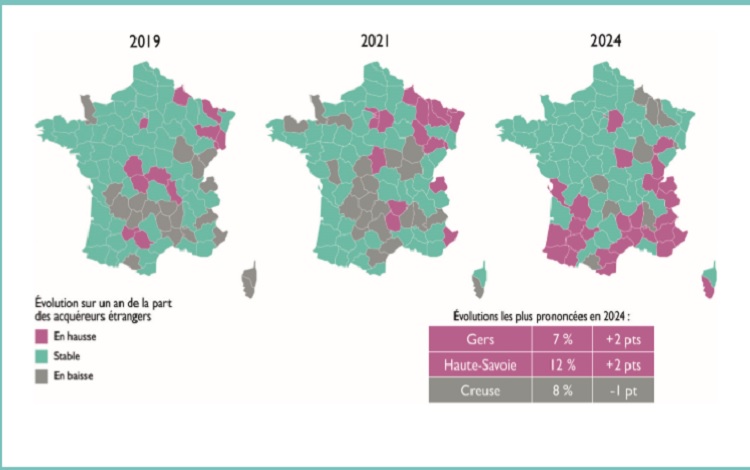

The notaires also provide a slither of information on the number of sales to foreign buyers, stating that there was a small increase in the year over 2023 in most departments.

In the departments of Gers and Haute-Savoie sales to foreign buyers progressed by +2% to reach, respectively, 7% and 12% of all sales.

In contrast, the department of Creuse lost ground, with foreign buyers accounting for 8% of sales, down -1%.

In the Alpes-Maritimes, sales to international buyers accounted for 13% of sales, compared to 9% in 2021 and 8% in 2019.

The graphic below shows the movement up or down or stable in each department for 2019, 2021 and 2024.

Subscribe to read this article

To read the full article you need to take out a premium subscription for €25/year.

A premium subscription will also give you unrestricted access to the complete back catalogue of our articles.

You can see the full catalogue of articles at France Insider News.

Subscribe to Premium for €25 a year →Already a subscriber? Sign in.

— or —

If you are not ready to take out a premium subscription, receive the headlines to our articles free of charge by entering your email address below.

More Property Market articles from France Insider