Barely a day passes in France without a headline warning about the parlous state of the housing market, with concern being expressed about a potential propery market 'crash'.

The French daily Les Echoes recently claimed that "la France traverse une grave crise de l'immobilier", Crédit Agricole have reported on the prospect of “an abrupt turnaround in the value of real estate”, whilst other experts report a "crise sans précédent".

Even the French public are doom-laden (what's new?), with a large majority in a recent poll expressing fears about their own housing prospects.

Several English-speaking news services in France have also echoed the noise, with one paper recently screaming 'Why France has a Property Crisis'.

A closer look suggests that whilst since the last quarter of 2022 the market has slowed, the indications are that things are simply getting back to normal, after the excesses of the past few years.

Sales

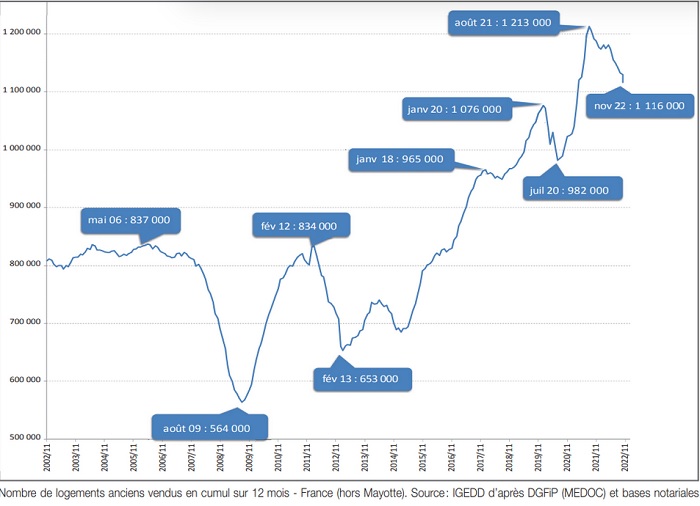

According to recent projections from notaires and FNAIM, sales of existing property are expected to dip under 1 million this year, down from around 1.2 million in 2021 and over 1.1 million 2022.

Nevertheless, if viewed over a longer period, the slowdown in sales is more of a return to the same levels of activity before the pandemic, rather than a violent change in the market.

The graphic below shows the number of sales each year since 2002. As can be seen, the period since 2019 has been unprecedented, and on a historic basis annual sales are normally around 850,000.

Interest Rates

A contributory factor to the fall in sales is the cost-of-living crisis, and the consequent rise in interest rates to combat inflation.

Whereas in March 2022 buyers could get a mortgage for around 1%, today the rate is over 3%, arguably pushing many first-time purchasers out of the market and preventing existing owners improving their current housing situation.

Once again, however, it is easy to overstate the case, for the era of free money over the past few years has been quite unprecedented and we are now seeing a return to more normal market rates.

The negative impact of increased rates may also only be a temporary shock because wages are rising, unemployment is down, and there are signs that inflation is beginning to abate.

The Bank of France recently addressed the impact of interest rates, stating that since the second half of 2022, there has been “a normalisation of the production of new housing loans.”

Although as a result of tighter regulation the banks have tightened up on access to loans, the Bank of France point out that “In April 2023, just over €12 billion of new housing loans were granted by banks in France, down from a peak of €20 billion per month during 2021, but at a level that seems to be stabilising well above the amounts observed during the decade 2005-2014, which was on average €9 billion a year".

They state that "all other things being equal" the decline in rates combined with the increase in borrowers' incomes was more than offset by the rise in prices, so that purchasing power would have decreased if banks had not extended the duration of loans.

Prices

Reliable information on the movement of prices is less readily available, mainly due to the delay in gathering and analysing the statistics.

However, with the reduction in the volume of sales, the scant information that has been published indicates that prices are generally heading south, although not dramatically.

Prices in Paris have (rightly) been falling for months, but the notaires are only forecasting a fall of -5% in the year. In the regions the notaires were reporting in April a ‘progressive deceleration’ of prices, with indications that in some areas prices were falling marginally. Overall, in Q1 of this year, INSEE, the French national statistics agency, reports that prices fell by -0.2%, although over a year they rose +2.7%.

FNAIM reported earlier this month that over the past 3 months prices had fallen in the regions on average by -0.9%. However, there is no geographical analysis of this figure and there are counter indications that in many rural areas prices are either stable or still rising. Similarly, their own predictions are that prices will fall on average by -5% over the year.

Any prospect of a significant fall in prices seems remote, due to an improving economy, a strong social security system, the fixed rate basis on which most mortgages are taken out and the 'safe haven' status of property in France.

New Build

Other commentators have pointed to the slowdown in the new build market and the crisis this is creating in obtaining access to the market.

Once again, however, it is necessary to set it context. According to the government, although new housing construction began to decline in the second half of 2022, there been over 400,000 planning approvals for new homes and over 350,000 housing starts, figures which are down on the years immediately prior to the pandemic, but above average over the past ten years.

According to the government, in order to meet housing requirements there needs to be between 300,000 and 350,000 new units a year, a figure which is being achieved.

The problem is not that there is insufficient new housing, but that they are being built in the wrong places, with much of it in green-field sites outside metropolitan areas, rather than in existing urban areas. And not enough of it is low-cost.

As we have reported previously, if there is a housing crisis in France it is primarily because prices in many cities are too high and a substantial percentage of the existing housing stock is not fit for purpose.

The problem is one that the government have rather belatedly started to tackle, by allowing (encouraging?) house prices to fall, removing tax incentives for new builds, imposing new controls on development in the countryside, improving access to the rental market for low-income households, reducing incentives for holiday lettings, and focusing more resources on the rehabilitation of the existing stock, mainly through grants for energy conservation. Thus far, the steps are only tentative, but if strengthened and maintained, far from a crisis, together they could bring about a far more equitable and sustainable market.

Related Reading: