According to the notaires, after a more active autumn period, the end of last year was marked by a clear loss of momentum: prices are broadly stable, transaction volumes are easing, and buyers are increasingly cautious.

This pause is partly seasonal but the notaires consider it also reflects deeper uncertainty, fueled by domestic budgetary deadlock and geopolitical instability, encouraging many households to delay their decisions.

Priscille Caignault, a member of the board of the Conseil supérieur du notariat commented that, “After two years of sharp decline, the real estate market began its recovery in the last quarter of 2024, which continued in the year 2025. Our optimism remains measured in view of the political, economic and geopolitical uncertainties that continue to weaken the prospects of the real estate market and that do not allow a frank restart. The French have a certain appetite for stone. But they are sensitive to a stabilised economic and political environment, a guarantee of confidence.”

It is a view shared by Guillaume Martinaud, President of the estate agent chain Orpi who stated, "Nothing is won. The political instability and geopolitical situation that we have been experiencing since September 2025 are already beginning to weigh on the market and are being read in the end-of-year figures.”

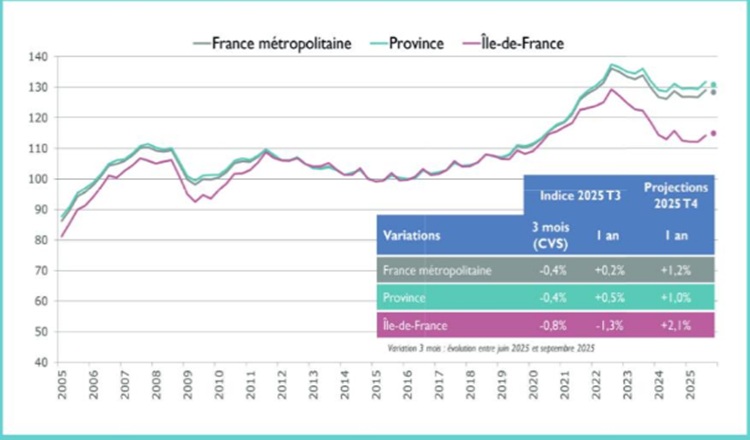

The graphic below from the notaires shows the movement in prices over the past 20 years.

While the anticipated adoption of the 2026 budget and the stabilisation of interest rates are expected to revive real estate projects in the months ahead, transactions may temporarily continue at a reduced pace.

One of the most striking findings of a recent survey of buyers is the growing number adopting a wait-and-see approach. Their share rose from 30% at the end of August to 44% in November. At the same time, the proportion of pessimistic respondents increased from 43% to 57%.

Nevertheless, the notaires consider these intentions remain fluid. Potential buyers retain the ability to move quickly or delay purchases until the last moment, depending on political or economic developments.

This flexibility is underpinned by the unusually high level of readily available financial savings in France. Household savings currently total €6.43 trillion, with around 60% held in regulated savings accounts and life insurance products. With a savings rate approaching 20%, France ranks among the highest in Europe.

Interest Rates

While price stability provides some reassurance, borrowing costs remain a major constraint. Higher interest rates are particularly challenging for homeowners seeking to trade up. In France, mortgage loans are generally not transferable: an existing loan must be repaid and a new one taken out when purchasing another property.

For households that bought between 2016 and 2022, when mortgage rates were exceptionally low, at around 1% to 1.5%, this implies losing the benefit of low monthly repayments and refinancing at rates closer to 3% or 3.5%. As a result, residential mobility is slowing, reinforcing the cautious tone across the market.

Outlook for 2026

Looking ahead, the notaires, along with most other commentators, largely agree that 2026 will be a year of consolidation rather than strong recovery. Stable prices, modest activity and selective buyer engagement are likely to define the market.

In a survey, 58% of notaires canvassed estimated a fall in prices, 40% consider prices will remain stable, and 2% anticipate an increase in prices.

While improved visibility on fiscal policy and interest rates could unlock delayed projects, confidence will remain fragile, leaving the housing market balanced between resilience and restraint.

Related Reading: