All multi-risk house insurance policies in France make full provision for damage caused by natural disaster (catastrophe naturelle), such as a drought, avalanche, earthquake, or flooding. Damage caused by fire, storms, hail and snow is not covered by the 'CatNat' scheme, but by standard insurance cover.

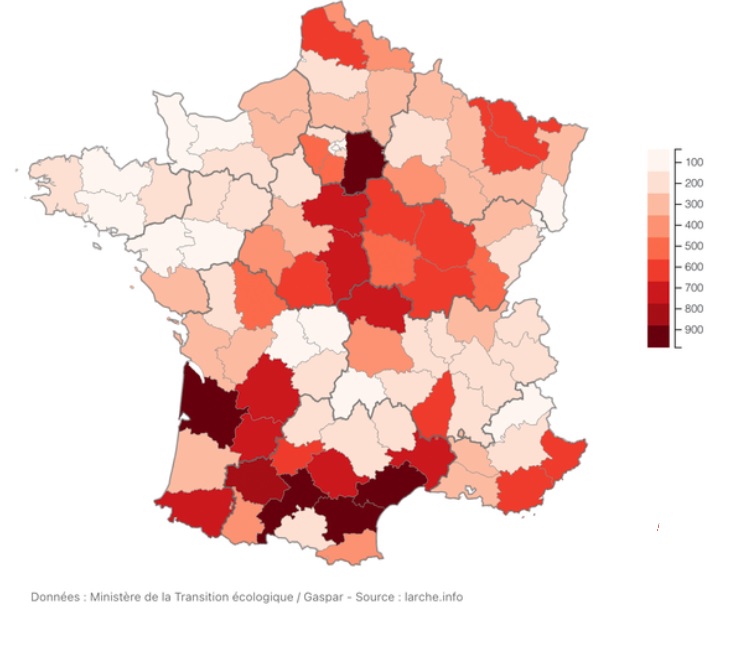

Over half the homes in France are exposed to the risk of a natural disaster in one form or another. The graphic below shows those areas where natural disasters have occurred to 2021, and the number of disasters since 2011.

CanNat insurance cover is provided via the aegis of state reinsurance, for incidents which are considered to be non-insurable, when the government steps in as the insurer of last resort, picking up around half of the bill, alongside the insurers.

The scheme is funded by a premium on insurance policies. The rate of this premium for house insurance increases in 2025 from 12% currently to 20%. This is the first increase since 2000. A parliamentary committee recently recommended that the premium needed to continue to rise each year as the reinsurance scheme was running at a substantial deficit and the number and scale of natural disasters was expected to rise significantly in the coming years, as a result of climate change.

Each year, these natural disasters occur in no less than 10% of municipalities, 3,500 per year, which generates €1billion in compensation paid.

Most of these claims are for subsidence and flooding, both of which are becoming more frequent due to climate change.

Nevertheless, although such protection is universal, the procedure for making a claim and obtaining compensation is complex, opaque and subject to several hurdles.

In the first place, the clause is not triggered until there is an official declaration of a catastrophe naturelle in the area by the government, and no claim can be made unless the local council submitted an application. The decision to declare a disaster is based on the intensity of the disaster, not the scale damage that will have been caused.

There is normally considerable delay by the government making a decision, and even if a favourable decision occurs, homeowners only have 10 days to submit their claim from publication of the decree.

If your local authority does not advise you of the decision, you risk losing out on your right to make a claim to your insurer.

The arcane nature of the process has finally been recognised by the government who have now passed a new law to streamline it and increase the rights of homeowners.

Among other measures, it revises the various deadlines applicable to compensation by insurers, in the interest of the victims. The main changes as they affect policyholders are as follows.

Application by Local Authority

With regard to local authorities, the law extends from 18 to 24 months the period available to municipalities to submit their application for recognition of a natural disaster. This is to allow for those circumstances where the damage caused by the incident may not appear for a year or more (notably subsidence)

Decree

The decree declaring a natural disaster must present a decision "reasoned in a clear, detailed and comprehensible manner, and (mention) the means and deadlines for appeal as well as the rules for the communication of administrative documents, including expert reports on which this decision was based, under conditions set by decree".

The criteria for recognising a drought have been revised to take better account of the often slow and progressive nature of the problem.

Decision Period

The text shortens the decision period: the decree for the recognition of a natural disaster must now be published no later than 2 months (instead of 3) from the filing of the application for recognition in the prefecture.

Marginal Cases

In local authority areas which suffer regular periods of drought, but not so severe that it would warrant a declaration of a natural disaster, the law now makes it possible to recognise a natural disaster in municipalities which have suffered an abnormal succession of droughts of significant magnitude over the previous five years. Neighbouring areas, which do not meet the criteria for declaring a natural disaster may also, under certain conditions, be recognised.

Claim Period

It extends from 10 to 30 days the period available to the insured to make their claim after the publication of the decree recognizing the state of natural disaster.

Compensation

The period granted to the insurer to pay the compensation is reduced from 3 months to 21 days from the date they receive an claim or, more precisely, in the absence of an expert report, when they receive the estimated statement of the damage and losses suffered by the insured, or the date on which it receives the final expert report. It can be 1 month if the insured agrees that the repairs can be carried out directly.

Subsidence

In the event of subsidence caused following drought or soil rehydration, compensation must be used to finance repairs that resolve the problem, rather than simply contain it. That will normally involve underpinning over the use of tie-bars.

Emergency Accommodation

The text extends the scope of the CatNat guarantee to include emergency relocation costs where the property is the principal residence.

Professional Fees

Architect and other professional costs associated with the works (including soil investigation) are covered by the guarantee and must be compensated.

Repair Works

If compensation is paid, the insured is required to undertake the repairs works, provided a solution is possible and the cost of the works does not exceed the value of the property before the disaster. Where the cost of the works is superior to the value of the property, the insured is entitled to compensation in cash, to use in a manner they deem fit, either to buy another property or to rebuild on their land.

The work must be completed within 2 years, save where there is a delay in obtaining the necessary administrative consents.

Insurance Excess

Insurers will no longer be able to modulate the deductible amount from the claim, according to the number of hazards in municipalities without a natural risks prevention plan - Plan de prévention des risques naturels prévisibles - PPRN.

Until now, in the absence of PPRN, an upward modulation of the deductible was planned from the second natural disaster. If a municipality, for example, was hit four times by a flood (with recognition of the state of natural disaster), the deductible was quadrupled. The insured were therefore less and less compensated for each disaster as a punishment because the municipality is not covered by a PPRN.

Sale of Property

On the sale of the property the seller must inform the buyer of the natural disaster and the works undertaken.

Legal Action

The limitation period for policyholders to bring an action for compensation for damage caused by ground movement following drought has increased from 2 to 5 years.

<li><a href="http://www.french-property.com/guides/france/insurance/"><span style="font-weight: bold;">Guide to House Insurance in France</span></a></li>