One of the traditionally most robust and best performing investment products in France are French property investment funds called Sociétés civiles de placement immobilier - SCPI.

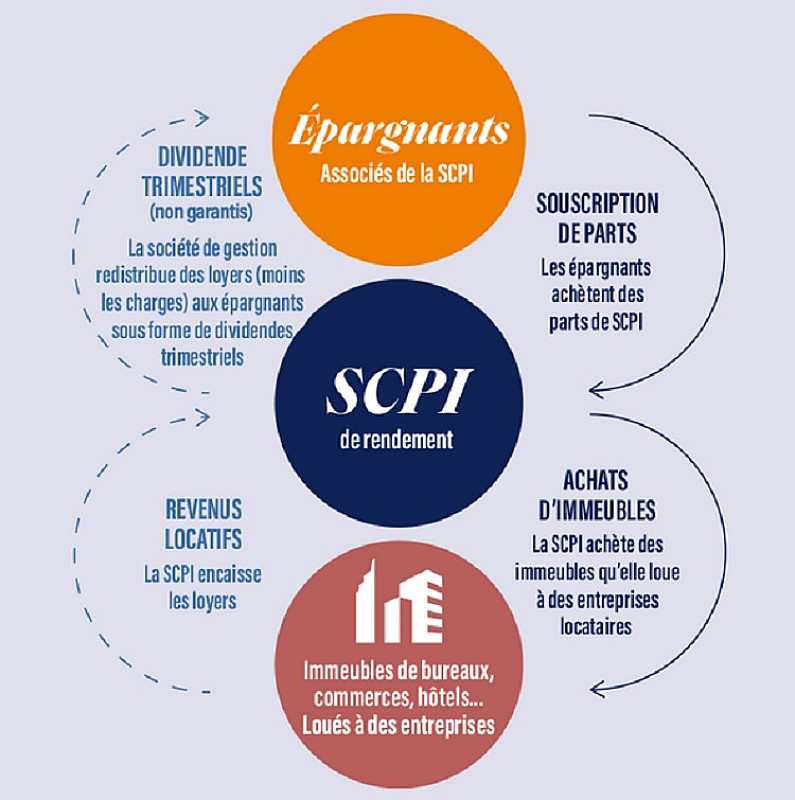

SCPIs are investment companies authorised to issue shares to institutions and the public, set up with the exclusive purpose of buying and managing commercial, industrial, and office property on behalf of the shareholders.

Their income comes from the rents that are charged to the commercial/public sector tenants, which is then paid out to shareholders in dividends, normally on a quarterly basis, pro-rate to the number of shares held.

SCPIs have been authorised by law in France since 1970, and under French law they are not able to be quoted on the French stock exchange. They are authorised and supervised by the French financial regulatory authority, the Autorité des marchés financiers (AMF).

The companies are managed by a professional management team (société de gestion) who collect the funds invested and undertake the acquisition, construction and management of the properties.

The returns have been well in excess of most other forms of investment, averaging over 5% gross pa during the past twenty years.

However, after more than a decade of euphoria, the SCPI’s are up against the downturn in the real estate markets and investors are losing confidence.

Since the beginning of 2023, several dozen funds, holding around half of the market have lowered the value of their shares, to reflect the fall in the value of the property. The government have also recently toughened the regulations to impose an obligation on the funds to value their portfolio twice a year.

Whilst the market is not collapsing, the impact in the use of commercial space in a post-covid, post-carbon era is bringing about a structural change. Most of the assets in the SCPIs are office space.

In the Ile-de-France, where most of the property is located, nearly 5 million square metres of office space is standing empty and in 2023 commercial business failures were up by 53%.

As a result, investors are seeing their returns and the value of their investments falling. Last year, on average, losses in value were -5.8%. Around €2 billion in shares are awaiting buyers.

Banks and insurance companies that own the properties are selling off some of their assets, often at a loss.

In such a climate, savers are reducing their exposure, with many seeking to surrender their investments. Some investors are also considering a group legal action against the financial advisors who promoted the funds.

To stem the leak, fund managers have taken temporary measures to block exits so that withdrawal requests are capped.

Nevertheless, as always of course it is a mixed market and despite difficulties amongst many of the major players, some of the more agile SCPIs have this year been able to raise their subscription price, and several new funds have entered the market.

Those considering entering the market need to consider that the entry price for a ticket is high, as are management fees. SCPI's are a long-term investment product, with ten years normally considered the minimum period necessary to hold the shares.

An SCPI needs to be distinguished from a Société Civile Immobilière (SCI), with which readers may be more familiar. The latter is merely a limited company that can be used for the purchase and ownership of French property.

Subscribe to read this article

To read the full article you need to take out a premium subscription for €25/year.

A premium subscription will also give you unrestricted access to the complete back catalogue of our articles.

You can see the full catalogue of articles at France Insider News.

Subscribe to Premium for €25 a year →Already a subscriber? Sign in.

— or —

If you are not ready to take out a premium subscription, receive the headlines to our articles free of charge by entering your email address below.

More Money articles from France Insider