Income tax in France is structured around five income bands, with different rates that apply on fractional income within each band.

In our article Income Tax in France 2026 we set out the tax bands and rates that apply in 2026 for income earned in 2025.

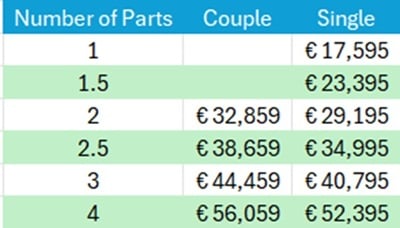

The table below shows the taxable income thresholds (after credits and allowances) that apply for residents before you pay income tax in France. The household is divided into 'parts', with an adult equating to one part and a child a half-part.

A couple with a taxable income below €32,859 would not have any income tax liability, whilst a couple with two children would not be liable for tax if their joint taxable income was less than €56,475. A single person living on their own would pay no income tax if their taxable income was below €17,595.

The figures, which are provisional at this stage, take account of the fact that if the tax due is less than €61 no tax is collected.

When official figures are available we shall publish the approximate income tax payable at different levels of income, for households whose taxable income is higher than these thresholds.

Those with a taxable income upwards of €250,000 pa (€500,000 for married couples and partners) are liable for a supplementary tax called contribution exceptionnelle sur les hauts revenus.

The table above excludes the social charges on pension income, which we covered in our article Social Charges in 2026.

Related Reading: